Road transport accounts for 12% of India's energy-related CO2 emissions and is also an important contributor to air pollution, which in 2019 is estimated to have caused over 1.6 million premature deaths in the country. India’s vehicle fleet continues to expand rapidly, overtaking Japan as the world's third-largest light vehicle market. It is the world’s largest two and three-wheeled vehicle producer and the second-largest bus maker. Within the light-duty vehicle market, the types of vehicles sold are rapidly changing, with SUVs accounting for over 40% of all sales in 2023 compared to just 16% in 2015, and is set to surpass 50% of all new vehicle demand by 2030 according to S&P Global Mobility forecasts. Increased sales of heavier and less fuel-efficient SUVs both globally and in India, are a major contributor to higher oil demand and greenhouse gas emissions. To meet India’s net-zero 2070 goal and reduce air pollution, India must decarbonize road transport, where electrification is widely recognized to play a key role.

India is one of the fastest-growing battery-electric vehicle (BEV) markets globally, with electric vehicles accounting for more than 6% of all vehicle sales in 2023. However, current trends highlight significant differences depending on vehicle type, with over 90% of India’s electric vehicles being two- or three-wheelers (motorbikes, scooters, and rickshaws). In 2023, over 50% of three-wheeler new registrations were electric, compared to only 5% of two-wheelers and 2% of four-wheeler passenger vehicles. Consequently, while India is rapidly electrifying its three and two-wheeler market, accelerating electric vehicle uptake for the passenger car market remains important.

In July 2023 the International Energy Agency (IEA) collaborated with the National Institution for Transforming India (NITI Aayog), an Indian government think-tank, to release the ‘Transitioning India’s Road Transport Sector’ report. It found that with increasing demand for private mobility and goods transported mostly by vehicles fueled with gasoline and diesel, CO2 emissions from Indian road transport could double by 2050. However, introducing ambitious policies could avoid 60% of expected CO2 emissions in 2050, saving India 70 million tonnes of oil equivalent (80% of the sector’s current energy needs). The report projected that while current policies would increase EV sales to 35% of vehicle sales in 2030, a higher target of 50% by 2030 is needed to meet India's net-zero 2070 goal. It further highlighted that the amount of CO2 avoided depends on how quickly India decarbonizes its coal-dependent power sector, with tailpipe CO2 emissions currently avoided by India's EV fleet roughly equaling the CO2 emissions indirectly created by power plants. As India decarbonizes its power sector, India's EV fleet is projected to avoid around 5 Mt of CO2 by 2030, rising to 110-380 Mt by 2050.

India is the world's fourth largest car manufacturer. It has set a national goal of achieving 30% battery electric vehicle (BEV) sales by 2030 for light-duty vehicles, 70% for commercial vehicles, and 80% for two or three-wheelers. There are three key federal policies to decarbonize light-duty transportation in India:

The Faster Adoption and Manufacturing of Electric Vehicles (FAME) scheme. The FAME scheme was launched in April 2015 under the National Electric Mobility Mission, to encourage electric and hybrid vehicle purchases by providing financial support. Its first phase ran for four years until 2019. The second phase (FAME II) is a 3-year subsidy program currently in place until March 2024 aimed at supporting the electrification of public and shared transportation (electric and ICE-powered hybrid buses, alongside electric two, three and four-wheelers), in addition to financing charging infrastructure. In August 2023, the Indian central government prepared the first draft for FAME III, with media reports suggesting the policy will be extended to electric trucks, bicycles and quadricycles. As of February 2024, the Indian government appears to not have officially extended the scheme.

Production-Linked Incentive (PLI) schemes that provide manufacturing incentives. The PLI scheme for the automotive sector was launched in September 2021 to boost domestic manufacturing of advanced automotive technology (AAT) products and attract investments in the automotive manufacturing value chain. The scheme has two parts: Champion OEM, which makes electric or hydrogen-powered vehicles, and Component Champions, which makes high-value and high-tech components.

Corporate Average Fuel Economy (CAFE) standards for passenger cars. Fuel economy regulations for vehicles with a gross vehicle weight of less than 3.5t were adopted by the Ministry of Power in 2015 as a fleet sales requirement for manufacturers. The regulation was implemented in a two-phased approach: in 2017 (Phase I) a manufacturer's sold vehicle fleet was to meet the target of 130g CO2/km, while Phase II (which took effect in April 2022) tightened the target to 113g CO2/km.

Across India, other researchers have suggested that future industry investment in BEVs and decarbonizing transport is stymied partly due to regulatory uncertainties. These include the lack of a binding zero-emission vehicle (ZEV) future sales mandate, and no roadmap to phase-down internal combustion engine (ICE) powered vehicles. In August 2023, a Centre for Science and Environment report noted that "there is no regulatory roadmap for the vehicle industry for achieving long term targets for fleet electrification" at the national level. Instead, federal policy appears to be primarily focused on incentive-based regulatory measures, which do not require meeting binding greenhouse gas emissions targets.

Regarding CAFE standards, a December 2021 International Council on Clean Transportation (ICCT) paper found that due to flexibilities incorporated into the policy, there had been no significant reduction in average fleet emissions from 2018-21. While India's CAFE standards have been set at 113g per CO2 from April 2022, no future standards have been confirmed. The IEA's 2023 ‘Transitioning India’s Road Transport Sector’ Report recommended a 55% reduction in corporate average fuel economy by 2035 to align India's transport sector with climate and air quality goals.

The IEA’s July 2023 report on India's road transport sector also found that "policy measures such as low-emission zones, stringent fuel-economy standards or zero-emission vehicle (ZEV) requirements can further accelerate EV deployment". It recommended strengthening policies for electrification, including the continuation of current incentive and favorable taxation policies, alongside considering ZEV sales mandates or registration restrictions for ICE vehicles. The report also recommended strengthening fuel economy standards, including introducing standards for two-wheelers, supporting the transition of heavy-duty vehicles, implementing a scrapping policy for the most polluting vehicles, and strengthening policies and mechanisms to improve access to EV financing.

Over the last few years, a series of historic climate reports from the Intergovernmental Panel on Climate Change (IPCC) have made increasingly clear findings on how to reduce road transport sector emissions in line with global climate targets. Using this, InfluenceMap defines "science-based climate policy" as the policies highlighted by the IPCC to deliver the Paris Agreement’s goal of limiting global temperature rise to well below 2°C, with efforts toward 1.5°C. Below is an overview of the IPCC’s most recent findings on transport.

IPCC’s Working Group III Report

According to the IPCC’s Working Group III report, published in April 2022, road transport was responsible for around 16% of global energy-related CO2 emissions in 2019. Other key findings in the report include:

Transport: The IPCC AR6 WGIII report found that “meeting climate mitigation goals would require transformative changes in the transport sector" (TS-67, 2) as CO2 emissions from transport could grow in the range of 16% and 50% by 2050" (TS-68, 23-24), potentially jeopardizing global climate goals as transport emissions have historically grown faster than other sectors.

Electric vehicles: The Summary for Policymakers (SPM) report notes that "electric vehicles powered by low emissions electricity offer the largest decarbonization potential for land-based transport, on a life cycle basis (high confidence)" (SPM-41, C.8).

Demand reduction: The SPM noted that “demand-side options and low-GHG emissions technologies can reduce transport sector emissions in developed countries and limit emissions growth in developing countries” (SPM-41, C.8). The technical summary found that “legislated climate strategies are emerging at all levels of government, and, together with pledges for personal choices, could spur the deployment of demand and supply-side transport mitigation strategies" (TS-69, 22-24).

Hybrids: While the full report recognizes that hybrids can "reduce emissions compared to ICEV by up to 30%, depending on the fuel" … "Because HEVs rely on combustion as the main energy conversion process, they offer limited mitigation opportunities", offering only a "suitable temporary solution". (10-40, 21-31). It also recognizes that "PHEVs may provide greater opportunities for use-phase emissions reductions for LDVs" with their lifecycle emissions between those of their ICEV and BEV counterparts of similar size and performance (10-40, 36-48, 10-41, 1-10). Yet the report noted that "ICEV, HEV, and PHEV technologies, which are powered using combustion engines, have limited potential for deep reduction of GHG emissions" (10-43, 25-26).

Biofuels: The full report highlighted that limited land and biomass resources accompanied by growing demands for food, feed, and fuels, together with shifting away from fossil fuels, creates substantial competition for land and biomass (Box 3, 12, 1304-1306). Consequently, biomass uses need to be prioritized, with the faster than anticipated adoption of electromobility for LDVs since AR5 partially shifting the debate around the primary use of biofuels from land transport to shipping and aviation (4.2.5.8, 10.3.1), with some short-term exceptions e.g. "in India, electrification, hydrogen, and biofuels are key to decarbonizing the transport sector" (4.2.5.8, 10.3.1). However, despite recognizing that biofuels may need to be targeted to ‘difficult-to-electrify’ sectors (6.4.2.6, 643-646), the IPCC AR6 report also stresses their considerable challenges. Large-scale production, high expansion rates (12.5.3, 1299) and biofuel crop monocultures (6.4.2.6, 645) heighten the risk of land clearing and negative impacts on food security and biodiversity. While such impacts can sometimes be mitigated through climate-smart land-use practices (Box 3, 12, 1304-1306), the report states that production needs safeguards to limit negative impacts on carbon stocks (7.6.3, 823).

Compressed Natural Gas (CNG): The full report noted that while fossil gas vehicles have lower air pollution emissions and produce no soot or particulate compared to conventional fuel-powered ICE vehicles, methane emissions from natural gas supply chains and tailpipe CO2 emissions "remain a significant concern". Consequently, natural gas as a transition fuel may be limited due to better alternative options and "regulatory pressure to decarbonize the transport sector rapidly" (10.3.1)

Vehicle type: The full report found that “if the trend towards increasing vehicle size and engine power continues, it may result in higher overall emissions from the LDV fleet (relatively to smaller vehicles with the same powertrain technology)” (10-41, 47-48, 10-42, 1). This direct link between higher energy usage and increased weight is highlighted in the figure below.

Using InfluenceMap’s established methodology for assessing corporate climate policy engagement, recently adapted to India, this chapter outlines the climate engagement, and top-line commitments on climate, of India's ten largest automakers, as well as their main industry association, SIAM.

InfluenceMap’s analysis of climate policy engagement by the Indian automotive industry focuses on the ten largest automakers by light-duty vehicle sales in India in 2023. In order of largest combined sales by their parent company, they are: Suzuki (through its Indian subsidiary Maruti Suzuki), Hyundai, Tata Motors, Mahindra & Mahindra, Toyota, Honda, Volkswagen, Renault, SAIC Motor and Nissan. Four of these are Japanese, two are Indian, two European and one Chinese-owned. Of these automakers, Mahindra & Mahindra is the most significant producer of three-wheelers, while only Honda and Suzuki are the only significant producers of two-wheelers, according to 2022 data.

The Society of Indian Automobile Manufacturers (SIAM) is the main industry association representing India’s automotive sector. Industry associations such as SIAM influence policy in the interests of their corporate members. As companies increasingly come under pressure from investors and the public to act on climate change, much of the negative advocacy traditionally undertaken by the companies is now outsourced to their industry associations. Globally, the most powerful advocacy groups are instrumental in shaping climate and energy policy in their respective regions. The UN Guide for Responsible Corporate Engagement in Climate Policy outlines the important role industry associations play. All ten of the automakers analyzed in this report are members of SIAM. The current president of SIAM is the CEO of Volvo Eicher Commercial Vehicles Ltd, while the Vice President is a senior executive from Tata Motors.

In 2023 over 1.5 million electric vehicles were sold in India, with two-wheelers (56%) and three-wheelers (38%) comprising 94% of overall electric vehicle sales. For four-wheelers, 80,003 electric cars and SUVs (5% of total EV sales) were sold, with sales more than doubling compared to 2022. In 2023, Tata Motors dominated four-wheeler electric vehicle sales with a 73% share of the market, followed by MG Motor (SAIC Motor) (12%) and Mahindra & Mahindra (5%). Out of ten analyzed automakers, only Mercedes-Benz signed the September 2021 COP26 Zero Emissions Declaration committing to the sales of all new cars and vans to be zero-emissions globally by 2040, and no later than 2035 in leading markets. Tata Motors subsidiary, Jaguar Land-Rover, also signed the declaration.

Many automakers have now committed to increase their production of battery electric vehicles within India itself, including automakers that currently produce no BEVs in India. For example, in October 2023 Suzuki announced plans for India to become its first global EV production hub through its subsidiary Maruti Suzuki, establishing a new production line for battery electric vehicles in Gujarat in the fall of 2024. In contrast, a February 2023 Economic Times report noted that Nissan was looking at "leveraging" India as a global base for manufacturing fossil-fuel-powered ICE vehicles while ramping up electric vehicle production in other regions. Potential differing strategies highlight the risk of automakers using India to sell their highest emitting fossil-powered ICE vehicles as other regions rapidly electrify amid more stringent climate rules. Similarly, BMW in February 2024 announced that it expects battery electric vehicles to account for 25% of its sales in India by 2025.

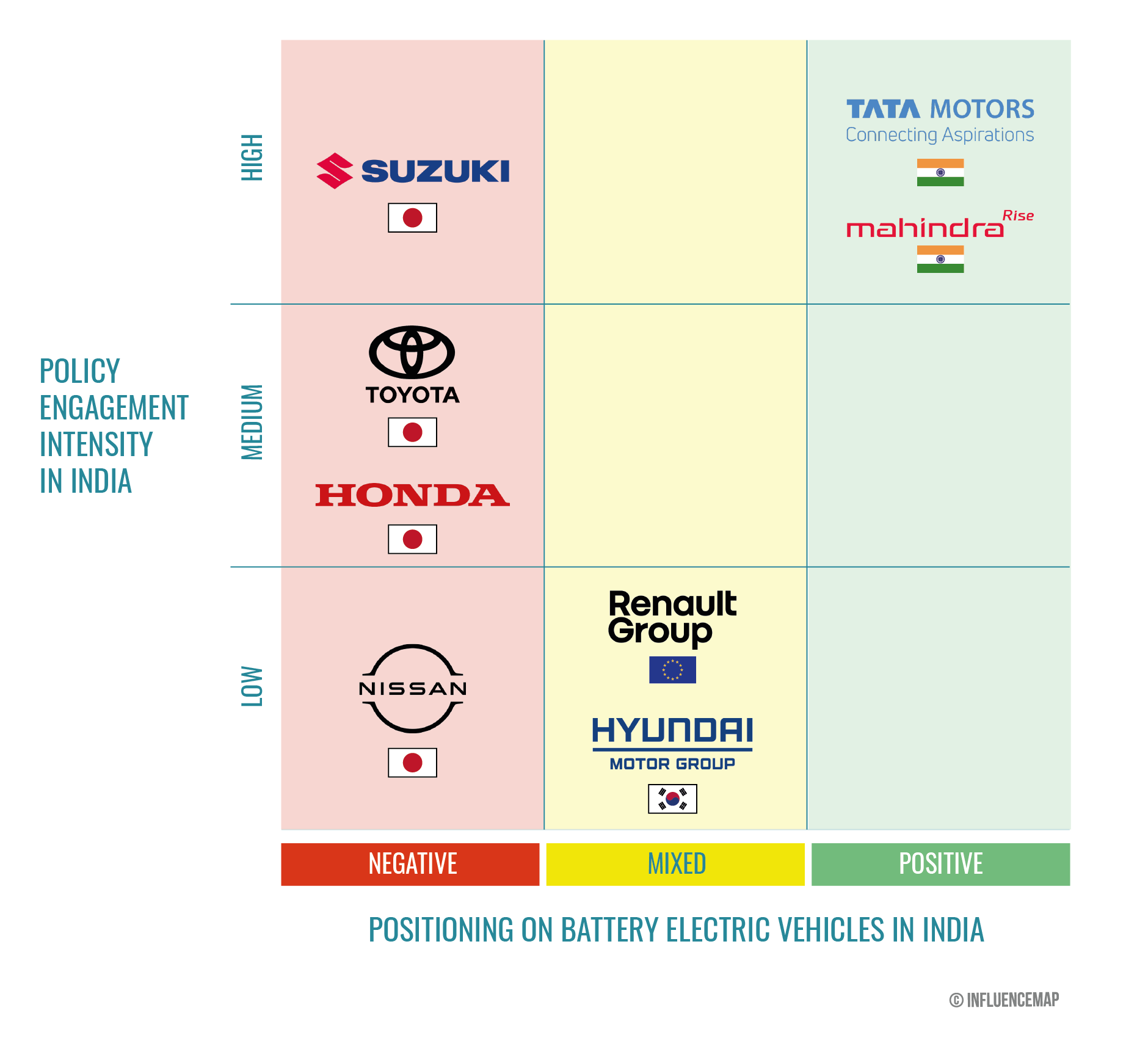

Figure 2 below ranks India’s 10 largest automakers by the percentage of total 2022 light-duty vehicle sales in India. Alongside this sales data, the global InfluenceMap Performance Band represents the full measure of a company’s direct and indirect engagement with climate policy worldwide, not just in India. A company's Performance Band is calculated by aggregating the following metrics: Organization Score (0-100%), indicating how supportive or oppositional a company is towards climate policy aligned with the Paris Agreement and the Relationship Score (0-100%), measuring how supportive or oppositional the aggregate of a company’s industry associations are toward climate policy.

There are also two metrics on India-specific climate policy advocacy. Firstly, 'Positioning on battery electric vehicles in India' indicates an organization's positioning on prioritizing battery electric vehicles to decarbonize road transport in the region. The policy engagement intensity represents the organization's level of engagement on climate-related policies in India, based on the number of evidence pieces found since 2022, ranked from low to high.

| Table Key | |||

|---|---|---|---|

| Negative positioning | A mix of negative & positive positioning | Positive positioning engagement | Unclear positioning |

| Automaker (key brands in brackets) | % of Total Indian Light-Duty Sales in 2022 1 | % of Indian light-duty four-wheeler battery electric sales in 2023 2 | % production that is ZEV in India by 2030 (S&P Global data) | InfluenceMap Performance Band (Global) | Positioning on battery electric vehicles in India | Policy Engagement Intensity in India 3 |

|---|---|---|---|---|---|---|

| Suzuki (Maruti Suzuki) | 42% | 0% | 11% | D | High | |

| Hyundai (Kia) | 21% | 3% | 16% | D+ | Low | |

| Tata Motors4 | 14% | 73% | 46% | D | High | |

| Mahindra & Mahindra | 9% | 5% | 15% | C+ | High | |

| Toyota | 4% | 0% | 30% | D | Medium | |

| Volkswagen (Skoda) | 3% | 0% | 10% | C- | No evidence | |

| Honda | 3% | 0% | 0% | D+ | Medium | |

| Renault | 2% | 0% | 16% | D+ | Low | |

| Saic Motor (MG) | 1% | 12% | No production | C- | No evidence | |

| Nissan | 1% | 0% | 11% | C- | Low | |

| Society of Indian Automobile Manufacturers (SIAM) | D | High | ||||

1 https://gomechanic.in/blog/annual-car-sales-india-2022/ 2 https://www.autocarpro.in/analysis-sales/ev-sales-in-india-charge-past-15-million-units-in-cy2023-stellar-growth-in-all-segments-118410 3 The Policy Engagement Intensity indicates the level of policy engagement by the company to decarbonize India's transport sector since 2022, measured by the number of evidence pieces found per group. 4 While Tata Motors overall scores a D, this is primarily due to the more negative global climate policy engagement of its subsidiary, Jaguar-Land Rover, in the UK and US. This contrasts with the more positive engagement from its parent company, Tata Motors, in India.

Tata Motors and Mahindra & Mahindra stated top-line support for the electrification of the Indian automotive sector in 2022-24. In January 2023 the Tata Motors Chair, Natarajan Chandrasekaran, was quoted by the Economic Times stating "we believe that the transition to electric mobility in India will happen much faster than what we are imagining". Money Control further reported a Tata Motors executive noting in September 2023 that "when the regulatory requirements become so stringent that a certain powertrain cannot exist, we will follow that". The Economic Times In September 2022 also reported Mahindra & Mahindra's Automotive Division President stated that "EV Is what really drives a greener environment", reporting that EV policies lets the company leapfrog to BEVs. In a January 2024 Reuters article, Mahindra & Mahindra's CEO stated regarding vehicles that "for us, electric is the future".

Maruti Suzuki appeared unsupportive of the electrification of the Indian automotive sector in 2022-24. Maruti Suzuki's Chair, R.C. Bhargava, criticized the use of EVs in India by emphasizing high power sector emissions from coal in a January 2023 interview with The Print. Bhargava also cited concerns around EV costs and high power sector emissions in India to push back against widespread EV adoption in statements appearing in a March 2022 Economic Times article. Similarly, in a March 2023 Money Control interview, Bhargava advocated for a "technology agnostic" Indian approach to decarbonization. Instead, Maruti Suzuki has consistently pushed for ICE-powered hybrids as a "medium-term" solution over BEVs, in statements such as those appearing in a February 2022 Hindu Business Line article. At the same time, the company has emphasized concerns around charging infrastructure and costs, and downplayed the GHG emissions reductions potential of BEVs in comments such as those by Maruti Suzuki's CTO in a July 2022 Economic Times article. Similarly, Suzuki's Global CEO was quoted by Bloomberg in May 2023 stating that EV's won't become popular in India until electricity is everywhere, noting that the world is "a little too focused" on EVs.

Japanese automakers advocated for ICE-powered vehicles, including hybrids, over the rapid electrification of the Indian road transport. For example, a January 2024 Economic Times article highlighted how "Toyota is lobbying" to reduce the Goods and Services Tax (GST) on ICE-powered hybrids purchases. In contrast, Mahindra & Mahindra, Tata Motors, and Hyundai advocated against reducing GST rates for ICE-powered hybrids vehicles, according to a January 2024 Reuters report. A Honda India Executive also advocated for ICE-powered hybrids over full electrification in September 2022 comments reported by the Economic Times, while a Nissan executive similarly appeared to push for Indian incentives to promote ICE-powered hybrids according to an October 2022 Fortune India report. An Economic Times article from March 2022 also reported that Maruti Suzuki’s Chair pushed for lower GST purchase taxes for CNG and ICE-powered hybrids, while in a June 2022 Hindu Business Line article, Maruti Suzuki's Chair stated that in India "EVs are not going to be a large part of car sales, irrespective of what other manufacturers are saying or planning.” Such advocacy appears aligned with the strategic pushback from Japanese automakers against climate regulations to promote BEVs globally (see InfluenceMap’s Automotive Sector and Climate Report) and regionally (see InfluenceMap’s FCAI and Australian Climate Policy Report).

Indian automakers are increasingly embracing the shift towards full vehicle electrification in India. In both a February 2022 Hindu Business Line article and a September 2022 Economic Times article, a Tata Motors executive argued that hybrid technologies were being pursued "primarily to meet Indian CAFE standards,” instead promoting BEVs as the longer-term zero emission technology solution. Similarly, a Tata Motors January 2023 X (formerly Twitter) post appeared to support India's 2030 30% EV target. In the same September 2022 Economic Times article, Mahindra & Mahindra’s President stated that "the government's clear position with its EV-specific schemes lets the company directly leapfrog into the battery electric vehicles".

Automakers generally supported electric vehicle charging infrastructure policies. The Times of India in February 2024 reported comments from SIAM's President, Maruti Suzuki, and a Renault executive that endorsed government plans to supporting EV charging infrastructure. Similarly, January 2023 comments from a Tata Motors executive, reported by DNA India in January 2023, supported government expenditure on electric vehicle infrastructure.

The Indian automotive sector is engaged in advocacy to promote biofuels and compressed natural gas. In a January 2022 Mint article, a Tata Motors executive promoted the use of compressed natural gas (CNG) vehicles alongside electric vehicles. Similarly_,_ Suzuki's 2022 Sustainability Report, published in March 2023, expressed support for the continued use of CNG vehicles. A March 2022 Economic Times article reported that Maruti Suzuki's Chair advocated to reduce purchase taxes for CNG and to promote "bio-CNG" made from agricultural waste. Outlook India also reported in December 2022 that Maruti Suzuki was advocating to India's road transport and highways ministry for the "correct account of greenhouse gas emissions benefits of ethanol in CAFE", suggesting advocacy for flexibilities to account for ethanol-powered vehicles in India’s CAFE standards. Maruti Suzuki's CTO, in a July 2022 Economic Times article, also pushed for CNG and ethanol to decarbonize Indian transportation, further stating that "bio CNG is carbon-negative". Similarly, a Hyundai Motor executive appeared supportive of CNG-powered vehicles in India in a July 2022 Autocar interview.

The US ethanol industry is targeting the Indian market as a potential avenue for biofuels growth. The Renewable Fuels Association (RFA), the leading US ethanol industry association, has over 100 members, including ethanol producers and national corn associations. RFA has actively advocated for legislation favorable to the ethanol industry in the US, frequently pushing for the continued blending of ethanol in road transportation over a full transition to electric vehicles.

According to an April 2023 Reuters article, the US corn ethanol industry has suffered years of stagnant demand as a fuel for gasoline-blending, with the growth of electric vehicles likely to further impede demand. Consequently, Geoff Cooper, President of RFA, asserted that the ethanol industry must “be looking at new uses and new markets”. India appears to be such a market; in its 2023 Outlook report, RFA noted that as India moved towards a national E10 standard it “imported significant volumes from the United States” and in 2022, India received 7% of US ethanol exports. Furthermore, in September 2023, the US, India, and numerous other nations, launched the Global Biofuel Alliance which intends to “expedite the global uptake of biofuels”.

Notably, India has become a focus of attention for RFA’s pro-ethanol advocacy. In January 2023, RFA released a press release supporting India's achievement of its 10% ethanol blending target and describing ethanol as a “preeminent solution to mitigating the impending climate crisis”, while stressing the economic benefits of a transition to ethanol. Similarly, in response to the advancement of India's 20% ethanol blending target from 2030 to 2025, RFA released a January 2023 blog that appeared to support the target. The blog post described ethanol as “a key component in achieving” India’s net-zero emissions by 2070 goal and states that the US is a “key partner” in helping India achieve 20% blending by 2025.

This section summarizes the Indian automotive industry’s engagement on automotive climate policy, namely positions on FAME II and III, and CAFE standards, which appear to be the two policy areas attracting the most engagement from the sector. It’s important to note that InfluenceMap was unable to access detailed Indian regulatory consultation responses from automakers and relevant industry associations, so corporate positioning assessments have been made based on other publicly available evidence.

| Table Key | |||

|---|---|---|---|

| Negative positioning | A mix of negative & positive positioning | Positive positioning engagement | Unclear positioning |

| Automaker (key brands in brackets) | Position on FAME scheme in 2022-24 | Position on CAFE standards in 2022-24 |

|---|---|---|

| Society of Indian Automobile Manufacturers (SIAM) | ||

| Mahindra & Mahindra | ||

| Volkswagen (Skoda) | ||

| Saic Motor (MG) | ||

| Nissan | ||

| Honda | ||

| Hyundai (Kia) | ||

| Renault | ||

| Tata Motors | ||

| Toyota | ||

| Suzuki (Maruti Suzuki) |

There is widespread support from automakers to expand the FAME scheme. The Society of Indian Automobile Manufacturers (SIAM) advocated for the extension of the FAME scheme to increase EV penetration in a July 2023 Business Today article . It also disclosed that it had advocated to policymakers for the extension of FAME Phase-II, which includes purchase incentives for electric and hybrid vehicles, in its 2020-21 Annual Report, published in September 2021. Similarly, Mahindra & Mahindra (together with its subsidiary, Last Mile Mobility) expressed support for the FAME program in its 2022 CDP disclosure, and called for an extension to the FAME II scheme in a May 2023 Economic Times quote. A senior Tata Motors executive supported extending FAME II in a January 2023 interview with DNA India. Similarly, in January 2024 a Maruti Suzuki executive was quoted stating that "the FAME scheme, PLI scheme, I suppose can have some modifications but should continue" in the Economic Times. A May 2022 Outlook India article also reported that a Honda India executive advocated for lower ICE-powered hybrid taxes, stating that "Toyota, and Maruti Suzuki are among other leading carmakers lobbying with the government for a favorable policy push for hybrids under India's FAME scheme". This advocacy appears similar to a key InfluenceMap global automotive research finding that many automakers widely support EV incentive schemes (e.g. the US Inflation Reduction Act) despite opposing stricter regulations mandating emissions reductions more aligned with global climate targets.

Maruti Suzuki was unsupportive of fuel-economy (CAFE) standards in 2021-2024, but engagement from other automakers was unclear. An August 2021 quote from Maruti Suzuki's chair, R.C. Bhargava, reported in The Economic Times, appeared to support delaying the implementation of 2022 CAFE standards, emphasizing cost concerns. Similarly, in March 2022 a Maruti Suzuki executive was reported by The Economic Times stating that regarding CAFE standards raising vehicle costs, "as an industry, we are requesting some benefit (pushing back the regulation) on those kinds of points". A December 2022 Outlook India article also noted that Maruti Suzuki had requested the "correct accounting of greenhouse gas (GHG) emission benefits of Ethanol in CAFE" norms from the road transport and highways ministry. Similarly, the former chair of SIAM, Kenichi Ayukawa, noted in an Economic Times interview in March 2022 that "as an industry" they had pushed back on the CAFE standards regulation without a response from the government.

InfluenceMap has assessed recent engagement from key cross-sector Indian industry associations which suggests broad business support for continued EV purchase incentives, policies to promote EV charging infrastructure, and generally supportive positions on higher CAFE GHG emissions standards.

The Confederation of Indian Industry (CII) stated support for both the FAME and Production Linked Incentive scheme in an October 2023 blog post, and for expanding policies to rapidly expand EV charging infrastructure in India in a July 2023 press release.

The Associated Chambers of Commerce and Industry of India (ASSOCHAM) supported extending Phase-II incentives from FAME for both BEVs and ICE-powered hybrids for 3-5 years in an August 2023 ‘Electric Mobility’ report. In the same report, it generally supported increased Indian CAFE GHG emissions standards, alongside advocating for broader incentives and/or lower Goods and Services (GST) tax rates for ICE-powered hybrids alongside BEVs.

A June 2023 press release from the Federation of Indian Chambers of Commerce & Industry (FICCI) noted that industry at a FICCI roundtable with government officials “sought extension of FAME II subsidy scheme by another 5 years” from its March 2024 end date. In a December 2023 press release, FICCI stated it submitted its proposal to the Ministry of Heavy Industries for a five year extension highlighting the measures had "created positive momentum" for EV adoption in India. An FICCI report released in June 2023 alongside the roundtable also suggested mandating EV charging infrastructure in public parking, supported incentives for EV vehicle purchases, and appeared supportive of “tightening emission norms” for CAFE GHG emissions standards.